- Platform

- Web and Mobile App

- Duration

- 14 weeks

- Industry

- FinTech

- Read time

- 5 min read

In short

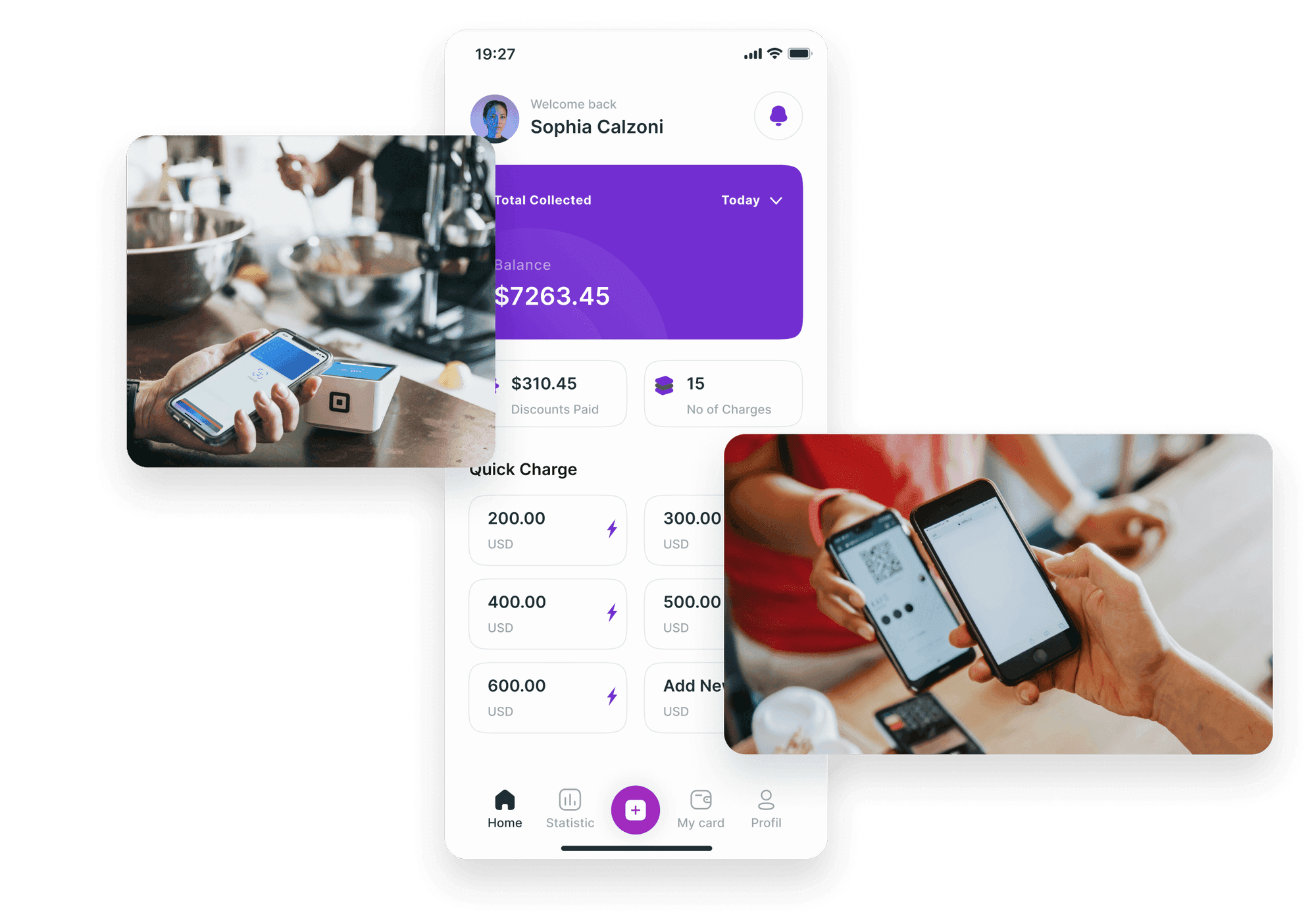

RaftLabs built a mobile POS application for a UAE FinTech operator (under NDA), enabling merchants and small businesses in the UAE to accept digital payments without traditional hardware POS infrastructure. The app supports contactless cards, QR codes, tap-to-pay, and link payments, and includes a real-time merchant analytics dashboard. The platform processed 10,000+ transactions in its first three months, achieved 5,000+ downloads with a 4.8-star Google Play rating, and delivered a 25% sales increase for merchants in remote areas. Built in 14 weeks using Flutter for cross-platform mobile, Next.js for the merchant web dashboard, Node.js, and PostgreSQL.

For small merchants in the UAE, especially those operating in remote areas or at markets, the problem with digital payments is not demand. Customers expect to pay by card or phone. The problem is access: traditional POS terminals require hardware investment, merchant account setup, and fixed infrastructure that smaller operators cannot justify or cannot get approved for.

A UAE FinTech operator came to us to close that gap. We built a mobile POS platform where merchants accept contactless cards, QR codes, tap-to-pay, and link payments through an app on their existing phone. No terminal hardware, no counter required. The platform processed 10,000 transactions in its first three months, reached 5,000+ downloads with a 4.8-star Google Play rating, and produced a 25% sales increase for merchants in previously cash-only locations.

before & after

What changed

- Small merchants and field sellers could not accept digital payments without purchasing hardware POS terminals and qualifying for merchant accounts, a cost and process barrier most could not clear

- Merchants in remote areas or at temporary locations had no option to accept cashless payments, losing sales to competitors with modern payment infrastructure

- No transaction data or analytics existed for merchants relying on cash: there was no visibility into sales patterns, peak times, or customer behavior

- Multiple payment method support (cards, QR codes, phone tap-to-pay) required multiple separate integrations that small operators had no technical capacity to manage

- Customer payment preferences had shifted toward contactless; businesses that could only accept cash were visibly at a disadvantage

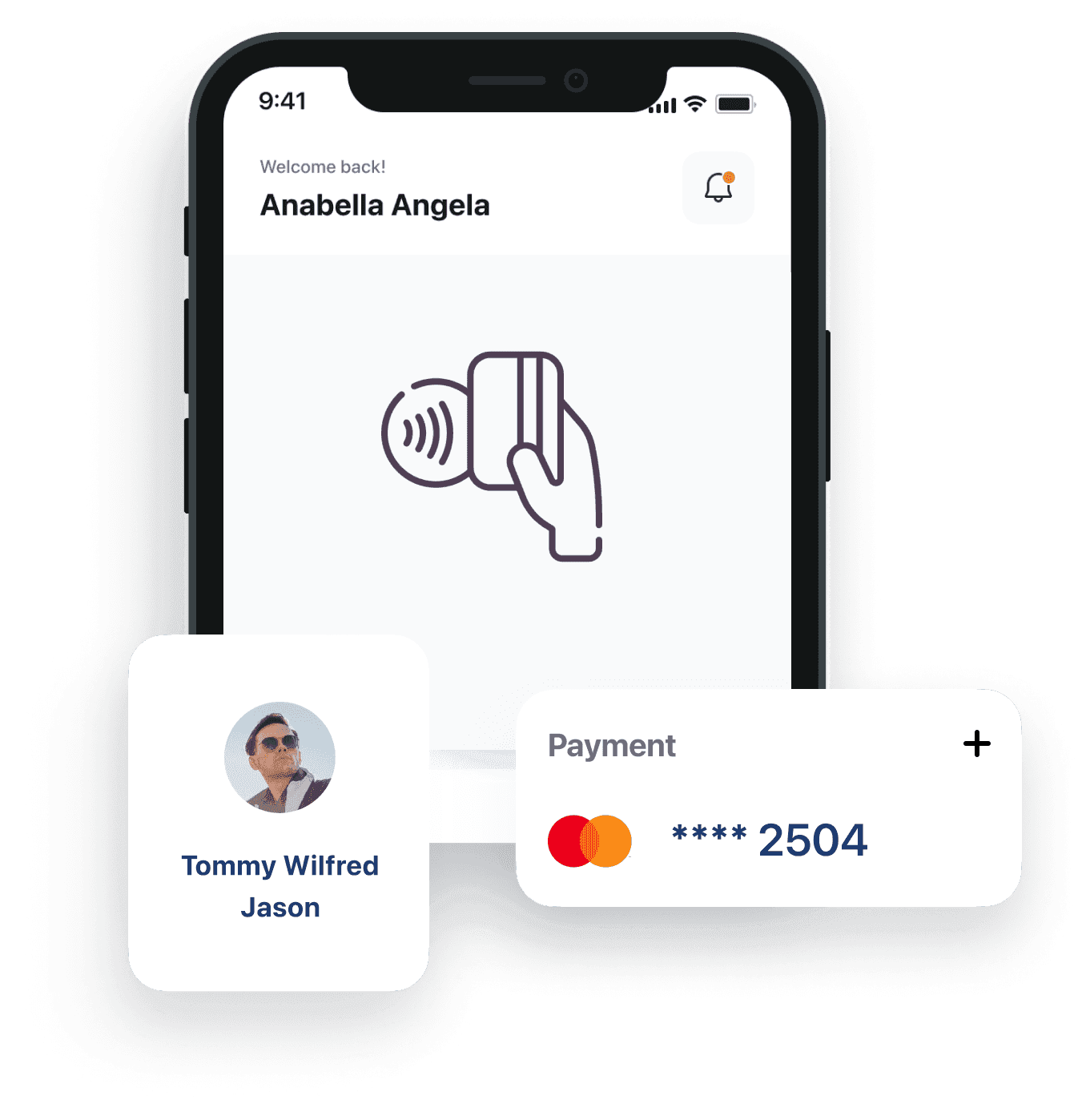

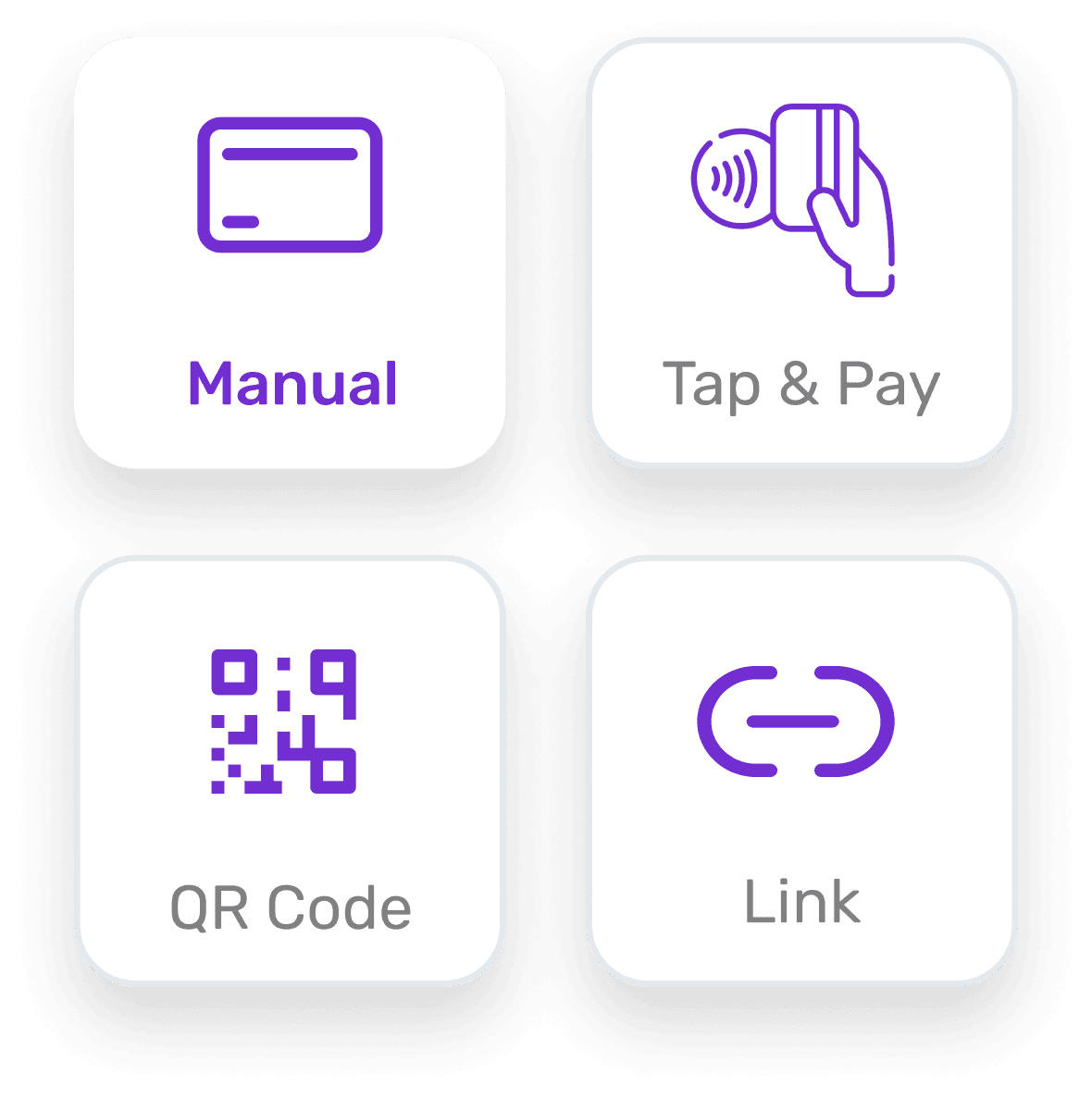

- Merchants accept contactless cards, QR codes, tap-to-pay, and link payments from a single app on their existing phone, with no hardware purchase required

- Field sellers, market vendors, and remote-area merchants accept digital payments anywhere with a data connection

- A real-time dashboard shows each merchant's transaction history, daily totals, payment method breakdown, and customer patterns

- New payment methods activate through the platform without requiring merchants to set up separate integrations or change their workflow

- Merchants previously limited to cash now compete on payment capability with larger retailers

What we had to solve

- 01

Meeting UAE payment compliance requirements without adding friction that merchants would abandon

Handling real financial transactions in the UAE requires compliance with Central Bank of UAE payment regulations, PCI DSS standards for card data, and security requirements that vary by payment method. Building a compliant payment flow is not a feature addition on top of a working app: it shapes the architecture from the start. The challenge was meeting each requirement without creating a merchant onboarding or transaction flow that felt more complex than the problem it was solving. A compliant app that merchants find too difficult to use fails just as completely as a non-compliant one.

- 02

Handling transactions reliably for merchants in areas with intermittent connectivity

A POS app that fails when the internet drops is worse than no POS at all: it trains merchants not to rely on it. Merchants in remote areas and market settings often operate on spotty mobile data. The platform needed an offline transaction queue that captured payment intent when connectivity dropped, held the record securely, and completed processing when the connection restored, without merchants needing to understand or manage that queuing behavior themselves.

outcomes

What we achieved

Small merchants had no affordable path to accepting digital payments. Hardware POS systems required capital investment and merchant account qualification that most could not access.

The payment tools available to small merchants were either expensive hardware or consumer apps not designed for merchant transaction management.

Merchants in remote areas were cash-only by default. No digital payment solution existed that worked without a fixed terminal, a stable internet connection, and hardware investment.

What clients say

Most clients stay.

Some say so on camera.

Three-year average engagement. Founders and operators describing the work in their own words. No marketing varnish.

RaftLabs helped us develop a mobile POS app that enabled smooth cashless payments. Their clear communication and collaborative approach kept the project running smoothly from start to finish, making the entire process efficient and successful.

Your merchants need digital payment capability but hardware POS is out of reach?

the build

What we built

The platform is built for merchants who need payment capability in the field, not for merchants who can assume a stable counter, reliable internet, and a fixed terminal.

Merchants accept tap, QR, or link payments, no separate hardware attachment needed

Merchants accept payments by tapping a card or phone to their device, scanning a QR code, or sharing a payment link. Each method routes through the same transaction record and appears in the merchant's dashboard identically. No separate hardware attachment is required for contactless: the phone's NFC chip handles the tap.

Payments process at a stall, a delivery, or a client site; offline payments queue and sync automatically

Merchants accept payments at a market stall, at a customer's location, or at a delivery handoff using the same app they use at a counter. Transactions queue offline when connectivity drops and process automatically when it restores. The merchant sees the same payment confirmation flow in either case, and the offline handling is invisible to both the merchant and the customer.

Merchants handle every payment type through one interface, no switching between apps

Customers choose from contactless card tap, QR code scan, NFC phone payment, or a shareable link sent via message. Each method completes through the same merchant interface and generates the same transaction record. Merchants do not need to manage separate integrations or switch between apps for different payment types.

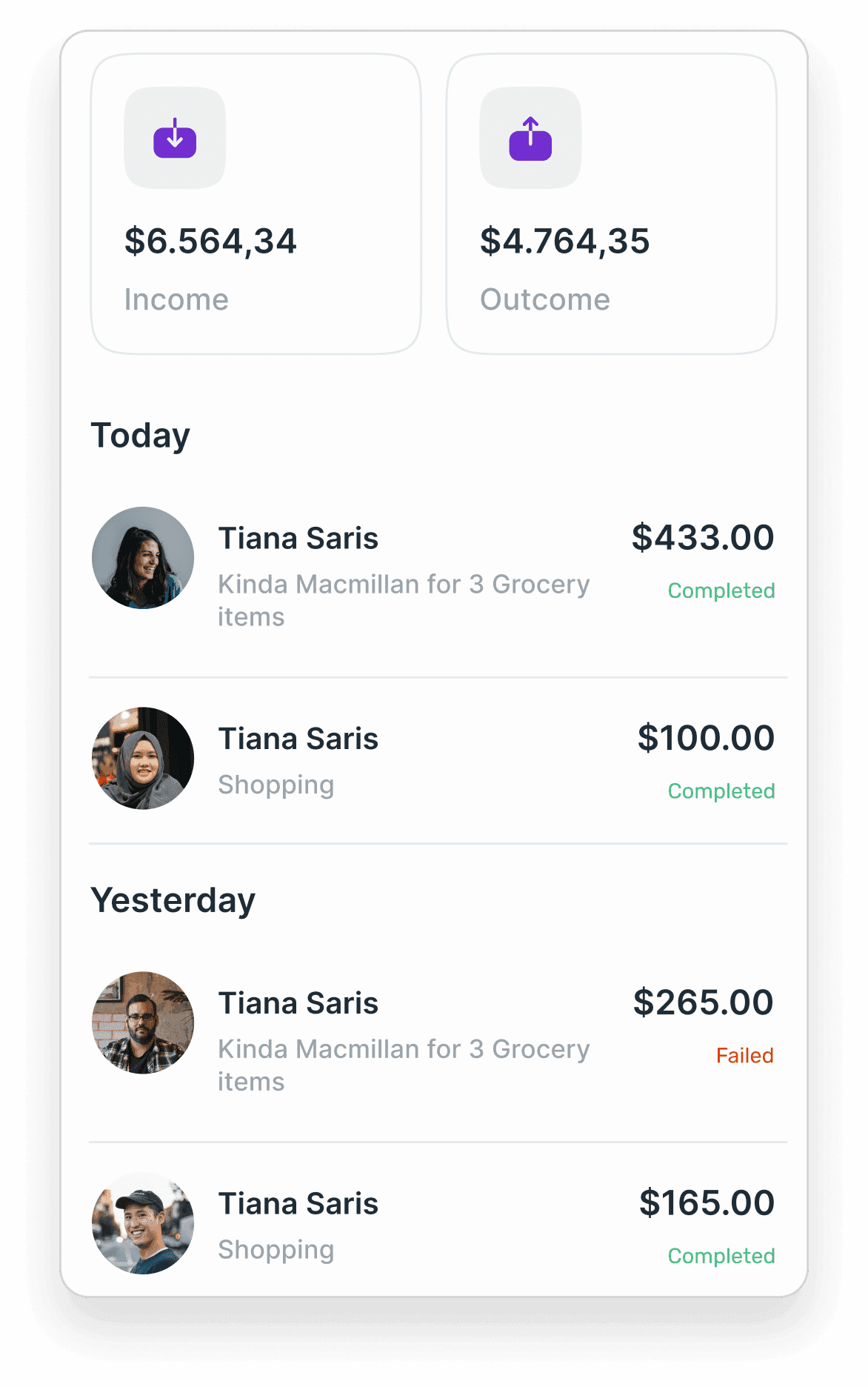

Merchants see daily totals and peak periods; operators pull settlement data for compliance

Merchants access a dashboard showing daily transaction totals, payment method breakdown, peak sales periods, and full transaction history with export. Operators see aggregate performance across their merchant base, identify volume trends, and pull settlement reconciliation data for compliance reporting, all from the same web interface.

Engagement

How we worked together

- 01Weeks 1–2

Discovery and scoping

We map the problem before writing code. Two weeks of technical audit, stakeholder interviews, and prototype — so both teams align on scope and risk before sprint one.

- 02Ongoing

Two-week Agile sprints

Each sprint ends with working software, not a status update. You review a real build, request changes, and approve before we move forward. No surprises at handover.

- 03Ongoing

Daily async updates

Slack for daily progress, Asana for task visibility, weekly video calls for decisions. You have full visibility without needing to attend every meeting.

- 04Final

Handover and warranty

Full code handover with deployment runbooks and documentation. Thirty-day warranty period for production issues at no extra cost.

stack

Why we chose this stack

- 01The payment app needed identical behavior on both Android and iOS across a wide range of merchant devices. Flutter's single codebase delivered consistent payment flows, camera access for QR scanning, and NFC tap-to-pay integration without maintaining two separate native builds.Flutter

- 02The merchant web dashboard (transaction history, analytics, settlement reports) needed fast server-side rendering so merchants on lower-bandwidth connections in remote areas could access their data without loading delays.Next.js

- 03The payment processing backend handles concurrent transaction submissions, payment gateway webhooks, offline queue processing, and real-time dashboard updates simultaneously. Node's event-driven model managed that concurrent I/O without thread management overhead.Node.js

- 04Financial transaction records require relational integrity and full audit history. PostgreSQL's transactional guarantees ensured that no payment record was lost or double-counted, and supported the settlement reconciliation queries the operator needed for compliance reporting.PostgreSQL

Common questions about mobile POS development

The platform is built to meet UAE Central Bank payment regulations and PCI DSS standards for card data handling. Card numbers are never stored on the device or the platform's servers: tokenization routes sensitive data to the payment gateway directly. QR code and link payment flows use expiring tokens that cannot be replayed. The compliance architecture was designed from the start rather than retrofitted, which is why regulatory approval did not delay the 14-week delivery timeline.

The app maintains an offline transaction queue that captures payment intent and holds the record securely on the device when connectivity drops. When the connection restores, the queue processes automatically and the transaction completes as normal. Merchants see a brief status indicator but do not need to take any action: the queuing behavior is handled by the app without requiring the merchant to understand or manage it.

The platform exposes a webhook and API layer that existing merchant accounting and inventory systems can connect to. Transaction events (completed payment, refund, settlement) fire webhooks that third-party systems can consume to update records automatically. For merchants using common accounting platforms in the UAE market, the integration reduces the manual reconciliation that otherwise consumes time after each trading day.

The current platform supports NFC card tap, QR code, tap-to-pay from a phone wallet, and shareable link payments. New payment methods are added at the platform level and become available to all merchants automatically: merchants do not need to update their app or change their onboarding to access new methods. The payment method layer was designed as an extensible module specifically because the UAE payments market was introducing new methods during the development period.

We delivered the Flutter app, Next.js merchant web dashboard, offline transaction queue, multi-method payment flows, real-time analytics, and payment gateway integrations in 14 weeks. The compliance architecture and offline queuing logic were the most time-intensive components: both required architectural decisions that could not be retrofit after the fact. A platform targeting a single payment method with no offline requirement would be faster. Contact us to scope based on the payment methods, markets, and compliance requirements your platform needs to cover.

Related work

More work like this

GrantHub indexes 1,600+ active grants across 21 countries so SMEs stop missing funding they qualify for

GrantHub gives businesses a single place to filter 1,600+ active grants and tax credits across 21 countries by country, industry, and business type.

Read case study

InvestIQ gets 5,000+ active users in 90 days by replacing five-tab research sessions with one feed

InvestIQ tracks every open and upcoming IPO, buyback, and OFS across Indian markets so retail investors never miss a deadline or a grey market move.

Read case study

Hospitality businesses cut inbound call costs by 80% with Call Eva

Call Eva answers every call 24/7 with natural-sounding conversation. Restaurants and hospitality businesses using it report 60-95% lower support call costs in the first month.

Read case study